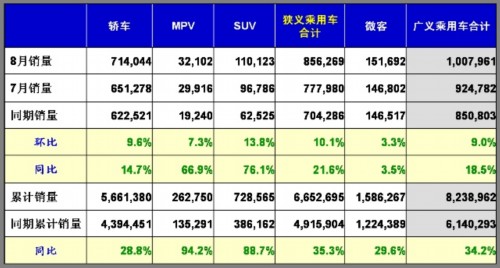

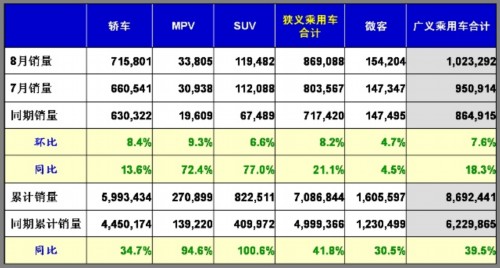

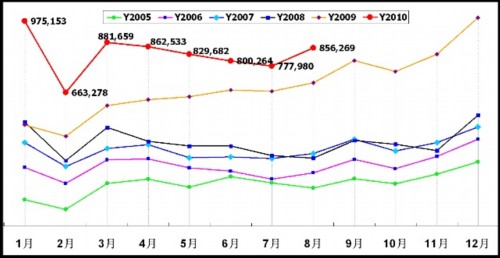

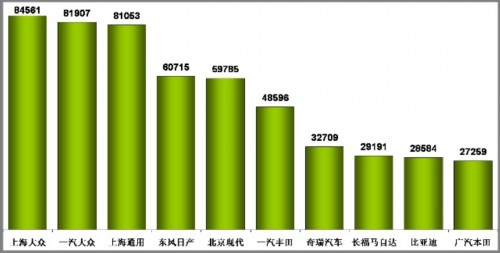

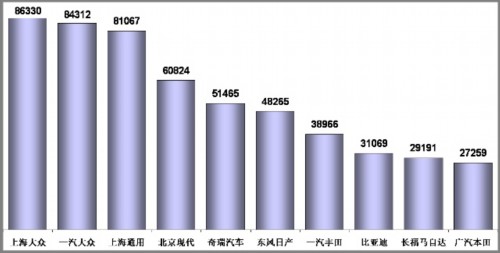

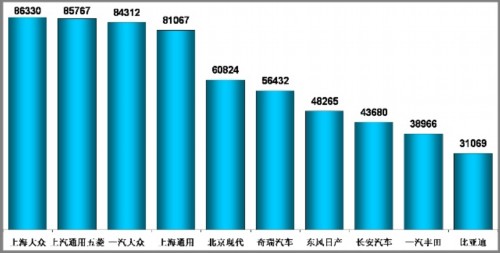

August production August wholesale sales table 2005-2010 monthly sales of passenger cars (car/MPV/SUV) Narrow Passenger Vehicle Manufacturer Sales Rank (August Domestic Sales Combined Number) Narrow passenger vehicle manufacturer sales ranking (August domestic and foreign sales wholesale number) General Motor Vehicle Manufacturer Sales Rank (August Domestic Sales Combined Number) General Motor Vehicle Manufacturer Sales Rank (August Domestic and Foreign Sales Wholesale Number) August Passenger Vehicle Market Review With continuous natural and man-made disasters, slowing down of international economic recovery and declining GDP growth rate in China, through hard work and vigorous promotion of the automotive industry, terminal sales in August have been greatly improved, and exports have also increased, indicating that the national economy as a whole The operation is basically good. Coupled with the fact that the number of inventories was accounted for by the CLUH last month, articles on hype stocks were reduced. In addition, the German cars continued to sell well. Toyota's car prices drastically reduced the price and caused a chain reaction of promotions. The role of sales growth, in recent years, wealthy families to buy a car before September in order to pick up the children to school or kindergarten, so that the market's August low market rebound month. Since August’s high-temperature holidays, equipment overhauls, and factory renovations resulted in more sales than production, it was not possible to conclude that the Chinese auto market experienced a reduction in inventory, which is basically the case in August each year. The declining sales of the auto market in July has already been in the end, but the market has continued to return to normal from the “blowout†period until the first half of next year. It also includes the negative growth of the market and the adjustment of the model structure. September Passenger Vehicle Market Outlook China's economic and automotive market trends are both high and low this year, and the rate of decline is slightly faster. Next year will be low and high. As the 4 trillion investment and many preferential policies expire, the last train effect will make economic growth in the fourth quarter. The decrease is smaller, so the key is to control the economic downturn in the third quarter. The national holiday arrangements for the National Day and the Mid-Autumn Festival will allow one more working day in September to be 22 days and one less working day in October to be 17 days. In this way, the working days in the third and fourth quarter are the same as last year, which can reduce the GDP growth rate in the third quarter by 1.6%, and it can also reduce the chain ratio in the first quarter of the next year. This shows that the government has also taken pains to arrange holidays and is very smart. Many do not understand. Insider's accusation is unreasonable. As for the production and sales volume of the automotive market, sales in September may increase by approximately 4.7%. In addition, many favorable factors of Jinjiu and the promotional role of energy-saving vehicle subsidies are fully utilized. However, in August, the market has already had a surplus of heat ahead. In September, the year-on-year Momentum market growth may be reduced. Imported cars "blowout" A new situation this year is the "blowout" of the imported luxury car market. The scale of this "blowout" is: From January to July this year, car imports totaled 460,000, which exceeded the total imports of the previous year and increased by 152% over the same period of last year. It is estimated that more than 700,000 vehicles will be imported this year, an increase of about 70%, and more than one million vehicles will be imported next year. If the policy does not change, the "blowout" of the imported automobile market will be a long-term trend. The sales of imported cars have contributed a lot to the economic recovery of developed countries; the price of some imported cars and the maintenance price are high; the foreign car oligopolists can make more profits; the large-displacement luxury cars are selling well, and the country is saving energy and reducing emissions. Contrary to policies, multinational car oligopolies have already reduced the proportion of domestic high-end cars in China, increasing the proportion of imported cars, and they are also welcomed by their own governments because of the benefits to their country’s employment, economy and tax revenue growth. Imported vehicles continue to "blowout" and will squeeze the domestic car market. Many high-end car technologies are advanced. If the joint venture reduces the proportion of high-end cars made in China, it is another technical occlusion of car oligopolies and it may not be possible for China’s auto industry to become stronger within 10 years. The reasons for the “blowout†are: China's upstarts are getting more and more competitive in buying cars, China’s luxury goods consumption is soaring, and multinational auto oligarchs have stepped up sales of luxury cars in China; the average price of imported cars is more than three times higher than that of domestic cars. The fiscal increase rate is extremely large, which may be tolerating the internal factors of the “blowout†of imported vehicles; China’s automobile consumption tax has serious loopholes, so that luxury imported vehicles can legally avoid high taxes. For example, if a car with a 3-liter supercharged engine imports a huge increase, it will pay only 12% of the automobile consumption tax, while a luxury car with un-supercharged engine of the same power should pay 40% of the automobile consumption tax. Only by revising the automobile consumption tax policy can we curb the "blowout" of ultra-luxury imported cars, but whether or not the changes will be known. The future of self-owned brand cars is worrying On July 15th, China's autonomous auto technology and product exhibition opened in Beijing, demonstrating that the hard work of domestic companies on the basis of national self-confidence has yielded fruitful results. The price is also very high, such as Chery, Geely, Great Wall, BYD. , SAIC, Jianghuai and other independent branded companies, research and development costs are greater than 10% of sales. When everyone praised the independent brand, the result of the research of the CCC was that the development prospect of the self-owned brand car was worrying. Because the state's policy on tilting its own brand was small, many models of the joint venture brand continued to seize the market in the market. In 2007, it won half the A0 class sedan market; in 2009, it accounted for more than 50% of the SUV market share; this year it took away the dominant position of the MPV market. At present, there is only A00-class passenger car and minivan market. The share of independent brands is greater than 50%. The market share of self-owned narrow-sense passenger vehicles has fallen month by month from 35.9% in January to less than 27% in August. Reduced market share by more than a quarter, so rapid decline is really worrying! We cannot allow everyone to buy their own brand of passenger cars, nor can they easily change the attitude of the auto industry in China. These are not conducive to the development of self-owned brands and the state of energy conservation and emission reduction. They can only be guided by policies. This is internationally As a precedent, nearly 30% of cars in Japan are <0.66 liters of minicars. China's encouragement to purchase small-displacement vehicles over the years is only a policy slogan, and so far there is no definition of small-displacement cars and self-owned cars. At the end of 2008, the Federation of Travel Unions proposed that the purchase tax preference be divided by the differential tax rate. The final decision is that the passenger vehicle below 1.6 liters is subject to a standard discount. Due to the edge of the policy, the 1.6-liter passenger vehicle is expanded. In the market, even the new Regal 1.6T C-Class sedan can also enjoy purchase tax subsidies. After the reduction in purchase tax at the beginning of this year, the market share of mid-to-high-end and premium sedans, SUVs, and MPVs increased, while the market for small-displacement cars declined. The market share of the A00 sedan in 2008 was 7.7%, and it was reduced to 7.3% in 2009. From January to August this year, the total number of cars dropped to 6.8% again, which has exerted tremendous pressure on the survival of domestic-funded enterprises. The plight of domestic-funded auto companies mainly comes from the country's auto market policy. The civil servants who formulate policies are internal experts. The top decision makers may be laymen, and domestic fraudulent lay companies can adopt policies that do not support domestic-funded enterprises because they will not buy A00-level policies. Cars, if they refer to Japanese policies for A00 cars, they must pay more taxes. Their patriotism is not strong either. Many developed countries' governments only use cars from domestic-funded enterprises, and the State Council stipulates that government-purchased autonomous brand cars account for 50% of the volume, but less than 30% on an amount-based basis. It can be seen that China’s auto market policy was played by the story of New Ye Gonghao Long. If this situation continues, it will take a long time for many private and state-owned auto groups to be dragged down. At present, auto listed companies are raising money for their own brands, and even China’s There is also a trend of full-scale joint ventures for commercial vehicles, so that domestic auto giants will change from manufacturing to investment companies in the tertiary industry. The actual control of the auto industry will be held in the hands of foreign auto oligarchs. At that time, China’s military and economic Security will be seriously affected! How far is the electric car from us? Electric cars can save more than 80% of gasoline costs if they use nighttime low-voltage electricity, but the key is to have a breakthrough in battery technology. Because "lithium batteries" are inferior to BYD's iron batteries, they have a large disadvantage in terms of life, safety, weight, and price. In the past two years, sales of F3DM have been very low. The most likely reason is that iron battery production consistency technology has not passed. It is hard to get a monopoly policy of leasing or replacing batteries. Computers and mobile phones have not used iron batteries. Great breakthroughs in science and technology require huge investments. Talented organizers and many hard-working R&D personnel must also have luck. We need to wait patiently. Since this year, the state and state-owned enterprises have invested the most financial resources and manpower in the world in the research and development of new energy vehicles. The international, national, industry, and local alliances of electric vehicles have emerged continuously. This is the largest venture investment since the founding of the People's Republic of China. The overflying of China’s economic development and the strengthening of China’s automobile industry as soon as possible are already a game that cannot be sustained. If all goes well, new energy vehicles will account for 5% of car ownership, and it will take 10 years. It is also necessary to use the soaring oil prices to accelerate the popularity. The slow recovery of the world economic and financial crisis means that there is no major breakthrough in the electric vehicle technologies that many countries expect! Mercury Lamp,Self-Ballasted Mercury Lamp,Vapour Discharge Lamp NANJING CAIDEAL PRODUCTS CO., LTD , http://www.chledlights.com